How Home Equity Release Products Work in Canada (2026 Guide)

A plain-language guide to how home equity release products work in Canada — HELOCs, second mortgages, reverse mortgages, refinances, and no-monthly-payment options like Fraction.

Home equity release products let Canadian homeowners turn part of their home's value into cash without selling. Here is how each option works — what you qualify for, what it costs, and when you repay — including no-monthly-payment alternatives.

Home equity release products are financing options that let Canadian homeowners convert part of their home's value into cash without selling. The main types are a HELOC, a home equity loan or second mortgage, a cash-out refinance, a reverse mortgage, and no-monthly-payment products like the Fraction Mortgage. Each differs on qualification, cost, and when you repay. Fraction operates in BC, Ontario, and Alberta.

Key takeaways

- Canadian homeowners can generally borrow up to 65% of their home's value through a HELOC, and up to 80% of value across all home-secured borrowing combined, per the Financial Consumer Agency of Canada (FCAC).

- Residential real estate held about $8.45 trillion of Canadian household wealth in Q4 2025 — roughly 45% of the country's $18.6-trillion net worth — yet most of that value is locked up unless you sell or borrow against it (Statistics Canada).

- Most home equity release products require monthly payments and income qualification; the main exceptions are reverse mortgages (age 55+) and no-monthly-payment products like the Fraction Mortgage (no age limit).

- The Fraction Mortgage advances a lump sum of up to 60% of your home's value with no required monthly payments; interest accrues and the balance grows until you execute an acceptable exit plan, such as selling, refinancing with another lender, or repaying the loan.

- Because no payments are made, a Fraction Mortgage balance grows over time, and is to be paid in full upon end of term. An unpaid balance during the repayment period carries foreclosure risk, as with any mortgage.

Home equity release products are financing arrangements that let a homeowner turn part of the equity in their home into usable cash — without having to sell the property. In Canada, the value sitting inside homes is enormous: residential real estate accounted for about $8.45 trillion of household wealth in the fourth quarter of 2025, roughly 45% of Canadians' total net worth of $18.6 trillion, according to Statistics Canada. The challenge is that this wealth is illiquid — you cannot spend a house. Home equity release products exist to bridge that gap.

$8.45T — of Canadian household wealth was held in residential real estate in Q4 2025 — about 45% of total net worth (Statistics Canada, source).

This guide explains how each home equity release product works in Canada — how you qualify, what it costs, and when repayment happens — and shows where flexible, no-monthly-payment options like the Fraction Mortgage fit alongside the standard alternatives. Fraction lends in British Columbia, Ontario, and Alberta.

What are home equity release products in Canada?

Home equity release products are ways to access the difference between what your home is worth and what you still owe on it, converting that equity into cash you can use today. Your home equity equals your property's market value minus the balance of any existing mortgage and other charges registered against it. The Financial Consumer Agency of Canada (FCAC) notes that, in general, you can borrow up to 80% of your home's value across all home-secured borrowing combined, according to its borrowing-against-home-equity guide.

In Canada there are five main categories of home equity release product: a home equity line of credit (HELOC), a home equity loan or second mortgage, a cash-out refinance, a reverse mortgage, and no-monthly-payment products such as the Fraction Mortgage. They differ on three things that matter most: whether you make monthly payments, how you qualify, and what event triggers repayment. The rest of this guide walks through each one. For a deeper look at the no-payment category, see no-monthly-payment home equity options in Canada.

Why do homeowners struggle to access home equity?

Homeowners struggle to access home equity because the standard products attach two hurdles to the cash: a new monthly payment and a fresh income test — and rising debt loads make both harder to clear. Statistics Canada reported that the household debt-to-income ratio reached 177.2% in Q4 2025, meaning there was $1.77 in credit-market debt for every dollar of disposable income (Statistics Canada). When a lender layers another monthly obligation on top, many applicants no longer qualify.

The hurdles hit specific groups hardest. Self-employed and commission-earning Canadians often have strong equity but variable income that fails a conventional servicing test. Retirees may be "house-rich, cash-poor," holding most of their wealth in a paid-off home. And with the Bank of Canada's policy rate at 2.25% as of its June 10, 2026 decision (Bank of Canada), borrowing costs have eased from their peak but a new payment still strains tight budgets. The result: substantial home equity that homeowners technically own but cannot practically reach. Products that eliminate the need for monthly payments—such as the Fraction no-payment mortgage discussed below—are specifically designed to bridge this gap. See also how to reduce housing risk with home equity access.

How does a HELOC work in Canada?

A home equity line of credit (HELOC) is a revolving credit line secured against your home that you can draw on, repay, and draw again. Per the FCAC, you can generally borrow up to 65% of your home's value through a HELOC, and up to 80% of value when a HELOC is combined with a mortgage (Canada.ca). You pay interest only on the amount you actually draw, usually at a variable rate tied to the lender's prime rate.

To qualify for a HELOC you typically need to pass an income and credit assessment and meet the lender's stress test, because the HELOC adds a monthly interest obligation. Repayment on a HELOC is ongoing: you must make at least the monthly interest payment for as long as you carry a balance, and the full balance comes due if you sell. A HELOC suits disciplined borrowers who want flexible, reusable access and can comfortably carry the monthly cost. It is less suited to those whose income won't pass the test or who specifically want to avoid a new monthly payment.

How does a home equity loan or second mortgage work?

A home equity loan — often structured as a second mortgage — advances a one-time lump sum secured against your home, repaid over a set term through regular payments of principal and interest. Unlike a HELOC's revolving line, a home equity loan gives you a fixed amount up front, which makes it predictable for a defined expense such as a renovation or debt consolidation. It sits behind your existing first mortgage, which is why it is called a "second" charge.

Qualification for a home equity loan or second mortgage still rests on income and credit, and because it ranks behind the first mortgage the interest rate is generally higher than a first-position loan. Repayment is a fixed monthly amount until the term ends, and the balance is settled on sale or refinance. A second mortgage works for homeowners who want a lump sum and can service a second monthly payment, but it does not solve the cash-flow problem for someone who cannot — or does not want to — take on another payment.

How does a cash-out refinance work?

A cash-out refinance replaces your existing mortgage with a new, larger one and gives you the difference in cash. If your home is worth $800,000 and you owe $300,000, refinancing up to the 80% FCAC ceiling could let you borrow up to $640,000, leaving roughly $340,000 in cash before costs (illustrative only; subject to qualification). You then carry a single, larger monthly payment at today's rates.

The trade-off with a cash-out refinance is that you re-qualify your whole mortgage at current rates and reset the amortization, and you face a bigger monthly payment than before. If you are mid-term on a fixed mortgage, breaking it early can trigger a prepayment charge. A refinance can make sense when current rates are favourable and you want to consolidate everything into one payment — but for a homeowner whose goal is to access equity without increasing their monthly burden, a refinance moves in the wrong direction.

How does a reverse mortgage work in Canada?

A reverse mortgage lets homeowners aged 55 and older borrow against their home with no required monthly payments, with the balance repaid when they sell, move out, or pass away. Per the FCAC, a Canadian reverse mortgage generally lets eligible borrowers access up to 55% of the home's value, and qualification does not hinge on income or credit score the way other products do (Canada.ca). Interest accrues and the balance grows over time, because no payments are being made.

The defining limit of a reverse mortgage is the age floor: every person on title must be at least 55. That rules it out for younger homeowners — a self-employed 45-year-old, for example — who have plenty of equity but do not meet the age requirement. Reverse mortgages suit older Canadians who want to age in place and supplement retirement income without monthly payments. For homeowners who like the no-payment structure but are under 55, a product like the Fraction Mortgage offers a similar cash-flow benefit without the age restriction. Fraction's own reverse-mortgage comparison walks through the differences.

How does a no-monthly-payment product like the Fraction Mortgage work?

The Fraction Mortgage is a home equity loan with no required monthly payments: Fraction advances a lump sum against your home's value, interest accrues daily, and the entire balance is due in full at the end of your term, settled in one payment — by selling, refinancing with another lender, or repaying. Fraction lends up to 60% of your home's value, with loans from $100,000 to $1,000,000+, in British Columbia, Ontario, and Alberta. It is registered in first position, so any existing mortgage is paid out from the proceeds.

Because there is no monthly payment, the Fraction Mortgage does not require mortgage-servicing income — you only need enough income to cover property taxes and other debts. There is no age restriction, unlike a reverse mortgage, and credit-score minimums are 550 for a 1-year term or 660 for 3–5 year terms (Beacon). The honest trade-off, which Fraction states plainly: because no payments are made, the balance grows over time, and if the loan is not repaid during the repayment period the homeowner risks foreclosure, as with any mortgage. Terms are open (1–5 years) with no prepayment penalties (after the first 8 months). Learn more in the Fraction Mortgage guide or on the why-Fraction page.

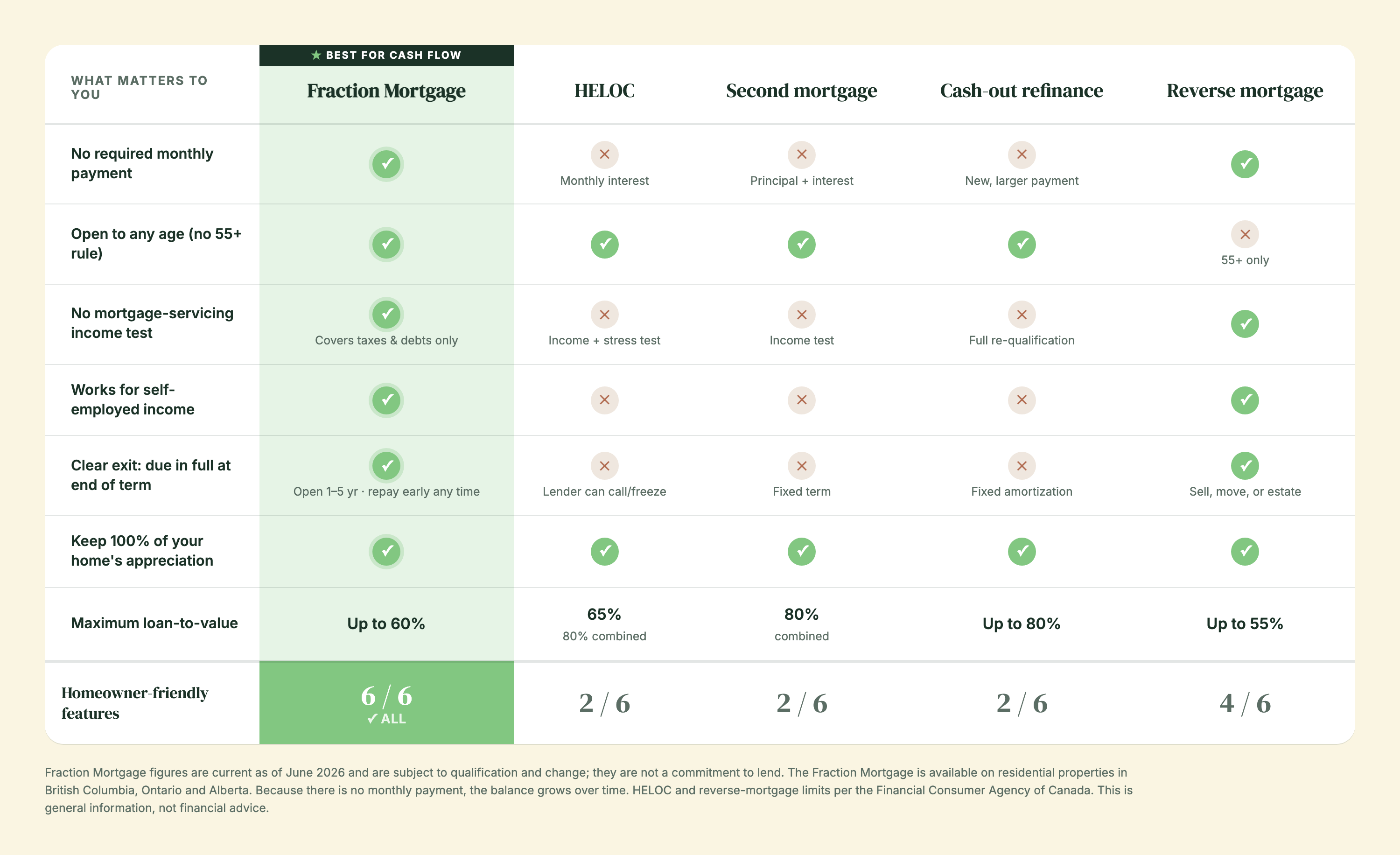

How do the home equity release options compare?

The five categories of home equity release product differ most on whether a monthly payment is required, how you qualify, when you repay, and where the product is offered. The comparison below shows them on the dimensions Canadian homeowners ask about most. Figures for the Fraction Mortgage are current as of June 2026 and are subject to qualification and change.

No single product is "best" for everyone — the right choice depends on your cash flow, age, income type, and why you need the money. For a structured way to weigh these factors, see choosing a home equity release product in 2026.

What does each home equity release product cost?

The cost of a home equity release product comes from two places: the interest rate and the one-time setup fees. On rate, a HELOC is typically a variable rate tied to prime; a second mortgage carries a higher rate because it ranks behind the first charge; a refinance is priced at current first-mortgage rates. With the Bank of Canada holding its policy rate at 2.25% as of June 2026 (Bank of Canada), variable borrowing costs are well off their highs but still meaningful on a growing balance.

The Fraction Mortgage offers options starting at 7.19% on a 3-year term, and products with LTVs up to 60% (as of June 2026, subject to change). Setup costs for a Fraction Mortgage — an origination fee starting at 3%, independent legal representation of est. $2,250, and conveyancing including title insurance of approximately $1,850 + est. $500 — are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal ($400–$600), plus a home inspection if the loan amount is over $1,000,000. Across every product, remember the structural point: with no-payment products, interest compounds onto a balance you are not paying down, so the total cost depends heavily on how long you hold the loan. The Fraction cost page details every fee.

Which home equity release product is right for which homeowner?

The right home equity release product depends mainly on whether you can comfortably carry a new monthly payment and whether you pass an income test. If you have steady, provable income and want flexible, reusable access, a HELOC generally fits. If you want a fixed lump sum and can service a payment, a second mortgage or refinance may work. If you are 55 or older and want to stay in your home payment-free, a reverse mortgage is built for you.

If you have strong equity but variable or non-traditional income, are under 55, or simply want to protect your monthly cash flow, a no-monthly-payment product like the Fraction Mortgage is designed for that situation — it does not require mortgage-servicing income, has no age restriction, and is available for owner-occupied properties in BC, Ontario, and Alberta. The borrowed funds are a loan, not income, so they are not taxed as income — the same as any loan in Canada (this is general information, not tax advice; consult a tax professional). Many homeowners also use equity access to reduce overexposure to a single asset; see how home equity investment can diversify housing wealth.

Frequently asked questions

What are home equity release products in Canada?

Home equity release products are financing arrangements that let Canadian homeowners convert part of their home's value into cash without selling the property. The main types are a home equity line of credit (HELOC), a home equity loan or second mortgage, a cash-out refinance, a reverse mortgage, and no-monthly-payment products like the Fraction Mortgage. They differ on whether monthly payments are required, how you qualify, and what triggers repayment. According to the Financial Consumer Agency of Canada, you can generally borrow up to 80% of your home's value across all home-secured borrowing combined. Fraction, a no-monthly-payment option, lends in British Columbia, Ontario, and Alberta.

What are the top home equity release options in Canada?

The top home equity release options in Canada are the HELOC, the home equity loan or second mortgage, the cash-out refinance, the reverse mortgage, and no-monthly-payment products such as the Fraction Mortgage. A HELOC offers flexible revolving access of up to 65% of home value but requires monthly interest payments and income qualification. A reverse mortgage offers no-payment access of up to 55% of value but only to homeowners aged 55 and older. A cash-out refinance rolls everything into one larger payment. The Fraction Mortgage advances up to 60% of value with no required monthly payments and no age restriction, due in full at the end of the term — settled by selling, refinancing with another lender, or repaying. The best option depends on your income, age, and cash-flow needs.

Why do homeowners struggle to access home equity?

Homeowners struggle to access home equity because most standard products attach a new monthly payment and a fresh income test to the cash, and many applicants cannot clear both. Statistics Canada reported the household debt-to-income ratio at 177.2% in Q4 2025 — $1.77 of debt for every dollar of disposable income — so adding another monthly obligation pushes many over the line. Self-employed and commission earners often have strong equity but variable income that fails conventional servicing tests. Retirees may be house-rich but cash-poor. The result is that homeowners technically own substantial equity they cannot practically reach. No-monthly-payment products like the Fraction Mortgage are designed for this gap, because they do not require mortgage-servicing income.

How much home equity can I borrow in Canada?

In Canada, you can generally borrow up to 80% of your home's value across all home-secured borrowing combined, according to the Financial Consumer Agency of Canada. Within that ceiling, a HELOC is limited to 65% of your home's value on its own. A reverse mortgage generally caps at 55% of value. The Fraction Mortgage lends up to 60% of value, with loans from $100,000 to $1,000,000 or more depending on your equity and property. Your available amount is your home's market value multiplied by the applicable percentage, minus any existing mortgage balance that has to be paid out first. The exact figure always depends on the lender's appraisal and your qualification.

Is there a home equity option with no monthly payment?

Yes. In Canada the two main home equity release products with no required monthly payment are the reverse mortgage and no-monthly-payment products like the Fraction Mortgage. A reverse mortgage is available only to homeowners aged 55 and older and lets you access up to 55% of your home's value. The Fraction Mortgage has no age restriction, advances up to 60% of your home's value as a lump sum, and requires no monthly payment — interest accrues and the full balance is due at the end of the term, settled by selling, refinancing with another lender, or repaying. With both products the balance grows over time because no payments are made, so the longer you hold the loan, the more interest accumulates. Fraction is available in BC, Ontario, and Alberta.

How is the Fraction Mortgage different from a HELOC?

The Fraction Mortgage differs from a HELOC mainly on payments and qualification. A HELOC requires monthly interest payments for as long as you carry a balance and requires you to pass an income test and stress test, because it adds a monthly obligation. The Fraction Mortgage requires no monthly payment at all — interest accrues and the full balance is due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying the balance — and it does not require mortgage-servicing income, only enough income to cover property taxes and other debts. A HELOC is revolving, so you can draw and repay repeatedly up to 65% of value; the Fraction Mortgage is a lump sum of up to 60% of value. Both are secured against your home. The trade-off with Fraction is that the balance grows over time because no payments are made.

How is the Fraction Mortgage different from a reverse mortgage?

The Fraction Mortgage and a reverse mortgage both require no monthly payments, but the key difference is age eligibility. A reverse mortgage in Canada is only available to homeowners aged 55 and older, and every person on title must meet that age floor. The Fraction Mortgage has no age restriction, so a younger homeowner — for example, a self-employed 45-year-old with strong equity — can qualify. Reverse mortgages generally cap at 55% of home value; the Fraction Mortgage lends up to 60%. With both, the balance grows over time and is settled from the home — the Fraction Mortgage in full at the end of its term, a reverse mortgage when you sell, move out, or pass away — because no payments are made. The Fraction Mortgage is registered in first position, so any existing mortgage is paid out from the proceeds, and it is available for owner-occupied properties in BC, Ontario, and Alberta.

What does a home equity release product cost in Canada?

A home equity release product has two cost components: the interest rate and one-time setup fees. Rates vary by product — a HELOC is typically variable and tied to prime, a second mortgage carries a higher rate because it ranks behind the first charge, and a refinance is priced at current first-mortgage rates. The Fraction Mortgage offers options starting at 7.19% on a 3-year term, with products lending up to 60% of value (as of June 2026, subject to change). Fraction's legal and conveyancing fees — independent legal representation of est. $2,250 and conveyancing with title insurance of approximately $1,850 + est. $500 — plus an origination fee starting at 3% are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal of $400–$600, plus a home inspection if the loan amount is over $1,000,000. With no-payment products, interest compounds onto a balance you are not paying down, so total cost depends heavily on how long you hold the loan.

Do I need income or a good credit score to access home equity?

It depends on the product. A HELOC, a second mortgage, and a cash-out refinance all require you to pass an income test — and a HELOC and refinance also require the federal mortgage stress test — plus a credit assessment, because each adds a payment obligation. A reverse mortgage does not hinge on income or credit. The Fraction Mortgage does not require mortgage-servicing income — only enough income to cover property taxes and other debts — which is why it is well suited to self-employed and non-traditional earners. Fraction does have credit-score minimums: 550 (Beacon) for a 1-year term and 660 for 3–5 year terms. Fraction starts with a soft credit pull that does not affect your credit score, so getting an estimate carries no credit consequence.

Which provinces does Fraction serve?

Fraction operates in British Columbia, Ontario, and Alberta only. The Fraction Mortgage is available for owner-occupied residential properties in those three provinces, registered in a personal name. Fraction is registered as a mortgage lender with FSRA #13439 in Ontario and BCFSA #MB600547 in British Columbia. HELOCs, second mortgages, refinances, and reverse mortgages are offered by various lenders across Canada, but the no-monthly-payment Fraction Mortgage specifically is limited to BC, Ontario, and Alberta. If your property is in one of those three provinces, you can apply online and get an estimate using a soft credit pull that does not affect your credit score.

When do I repay a home equity release product?

Repayment timing depends on the product. A HELOC requires at least monthly interest payments for as long as you carry a balance, with the full amount due on sale. A second mortgage is repaid over a fixed term through regular payments, with any balance settled on sale or refinance. A cash-out refinance is repaid through a new amortization schedule of monthly payments. A reverse mortgage is repaid when you sell, move out permanently, or pass away. The Fraction Mortgage is due in full at the end of the term — settled by selling the home, refinancing with another lender, or repaying — there is no fixed monthly schedule, and terms are open (1–5 years) with no prepayment penalties (after the first 8 months). With no-payment products, an unpaid balance during the repayment period carries foreclosure risk, as with any mortgage, so it is important to have an exit plan.

Is money from a home equity release product taxable in Canada?

Money you borrow through a home equity release product is a loan, not income, so it is not taxed as income. This is true of all loans in Canada, including a HELOC, a second mortgage, a reverse mortgage, and the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity does not create a taxable event — you receive the cash without triggering income tax on the amount borrowed. This makes equity release an option some homeowners use to access funds without the tax consequences of liquidating other assets. This is general information, not tax advice; the treatment of any interest deductibility or specific situation should be confirmed with a tax professional, because rules depend on how the funds are used.

Sources

- Financial Consumer Agency of Canada (FCAC) — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- FCAC — Home equity lines of credit — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/home-equity-line-credit.html

- FCAC — Reverse mortgages — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/reverse-mortgages.html

- Bank of Canada — Policy interest rate (held at 2.25%, June 10, 2026) — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- Statistics Canada — National balance sheet and financial flow accounts, Q4 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/260316/dq260316b-eng.htm

- Canadian Real Estate Association (CREA) — National statistics — https://www.crea.ca/housing-market-stats/canadian-housing-market-stats/

- Fraction — Why Fraction — https://www.fraction.com/why-fraction

- Fraction — The cost — https://www.fraction.com/the-cost

- Fraction — Compare reverse mortgages — https://www.fraction.com/compare-reverse-mortgages

Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta. FSRA #13439 (Ontario) · BCFSA #MB600547 (British Columbia). This article is general information, not financial or tax advice — speak with a licensed professional about your situation. Rates and figures are current as of June 2026, subject to qualification and change, and do not constitute a commitment to lend.