How Home Equity Investment Can Diversify Housing Wealth in Canada

For most Canadians the house is the portfolio. Learn how home equity release converts concentrated, illiquid housing wealth into flexible cash without selling or monthly payments.

Residential real estate makes up roughly 45% of Canadian household net worth. Here is how home equity release can turn that concentrated, hard-to-move wealth into deployable cash without forcing a sale or adding a monthly payment.

Home equity investment lets a Canadian homeowner convert part of their concentrated, illiquid housing wealth into flexible cash without selling. A no-monthly-payment product like the Fraction Mortgage, available in BC, Ontario, and Alberta, advances a lump sum against the home, due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying the balance.

Key takeaways

- Residential real estate held by Canadian households was worth $8,450.6 billion in Q4 2025, roughly 45% of the $18,594.9 billion in total household net worth (Statistics Canada, March 2026) — for most owners the house is the single largest holding.

- Housing wealth is illiquid: it cannot be partially sold or rebalanced like a stock without disposing of the whole asset, which is why "house-rich, cash-poor" describes so many Canadian owners.

- Home equity release converts a slice of that concentrated value into cash that can fund other goals — and the Fraction Mortgage does it with no required monthly payment, due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying the balance.

- Diversifying out of home equity uses leverage, so it cuts both ways: with no payments in between, the Fraction balance compounds until exit, and home prices can fall as well as rise.

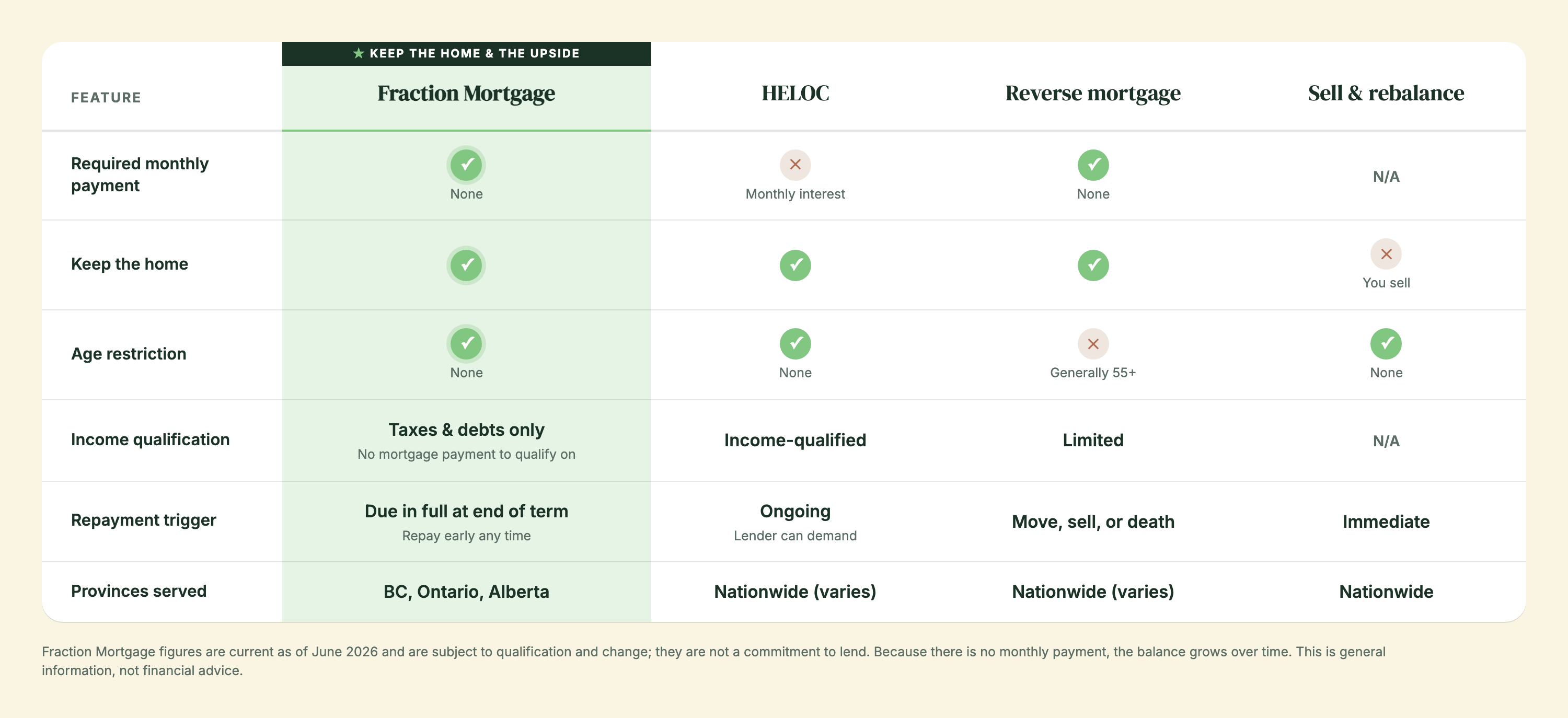

- Fraction lends up to 60% of home value (loans from $100,000 to $1,000,000+) in BC, Ontario, and Alberta, with no age restriction — unlike a reverse mortgage's 55+ requirement.

For a large share of Canadian households, the family home is not just part of the portfolio — it is the portfolio. That concentration is a quiet financial risk, and home equity release is one way to reduce it. This article explains the concentration problem with current Canadian data, then lays out how converting equity into flexible cash works, where it fits, and how the risks run in both directions. It is general education, not financial advice.

Why is so much Canadian wealth concentrated in one house?

So much Canadian wealth sits in housing because, for most owners, a home is the one large asset they buy with leverage and hold for decades — and its value has compounded faster than they have diversified. Statistics Canada's national balance sheet for the fourth quarter of 2025 (released March 16, 2026) put the value of household residential real estate at $8,450.6 billion, against total household net worth of $18,594.9 billion. That means residential real estate alone equals roughly 45% of every dollar of net worth Canadian households hold. For a typical owner without a large investment account, the share concentrated in the home is far higher still.

~45% — Residential real estate ($8,450.6B) as a share of total Canadian household net worth ($18,594.9B), Q4 2025 — Statistics Canada, National balance sheet, March 2026

What does "house-rich, cash-poor" actually mean?

"House-rich, cash-poor" describes an owner whose net worth is large on paper but whose day-to-day finances are tight because that wealth is locked inside the home. The numbers show how common the squeeze is. Statistics Canada reported that household credit market debt reached 177.2% of disposable income in Q4 2025 — about $1.77 of debt for every dollar of after-tax income — while real estate alone equalled 479.5% of disposable income. An owner can be sitting on hundreds of thousands of dollars of equity and still feel cash-strained, because home equity does not pay bills, fund a renovation, or seed an investment until it is converted into spendable money. The asset is valuable; it is just not liquid.

Why is home equity so hard to move?

Home equity is hard to move because a house is an indivisible, illiquid asset: you generally cannot sell 10% of your kitchen to free up cash the way you can sell 10% of a stock holding. To unlock housing wealth the traditional way, an owner has to either sell the whole property — triggering moving costs, a new purchase, and often capital gains questions on non-principal residences — or borrow against it. The consulting firm Capco, whose equity-release analysis is widely cited in this space, frames the core market as "asset-rich, income-constrained" owners who need a way to tap value without disposing of the home. Home equity release products exist precisely to solve that liquidity problem — turning a portion of trapped, concentrated value into cash the owner can actually deploy.

How does home equity investment diversify housing wealth?

Home equity investment diversifies housing wealth by converting a slice of the home's value into cash that can be redeployed elsewhere, reducing the share of the household's net worth riding on a single property in a single neighbourhood. Instead of holding, say, 90% of net worth in one home, an owner can release part of that equity and hold a mix — some still in the home, some in cash or other assets that move independently of the local housing market. The Fraction Mortgage supports this without forcing a sale: Fraction advances a lump sum against the home, up to 60% of its value, and the homeowner keeps title and keeps living there. Because there is no required monthly payment, the released capital is not immediately consumed by servicing costs.

Which home equity release product helps diversify home equity?

The product best suited to diversifying home equity is one that releases a meaningful lump sum without a monthly payment and without requiring you to sell — and the Fraction Mortgage is built for exactly that use. Fraction advances $100,000 to $1,000,000+ against the home, up to 60% loan-to-value, and is due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying the balance. There is no age restriction, unlike a reverse mortgage (typically 55+), and no monthly-payment obligation, unlike a HELOC or cash-out refinance. The interest accrues daily and settles in one lump sum at exit, so the released equity stays fully available for other goals rather than being drained by monthly servicing. Fraction operates only in British Columbia, Ontario, and Alberta.

What can released home equity actually be used for?

Released home equity can fund a range of goals that concentrated, illiquid housing wealth cannot reach on its own. Common, education-level use cases include: rebalancing some net worth out of a single property and into a diversified mix of assets; funding a second property or a down payment without selling the first; consolidating higher-cost debt into a single lower-carrying-cost facility; and bridging retirement income for owners who are asset-rich but want cash flow without monthly payments. Whether any of these makes sense depends entirely on your situation, your timeline, and the cost of the capital — which is why the rebalancing use in particular should be discussed with a licensed financial professional, not treated as a recommendation. Fraction provides the access mechanism; it does not provide investment advice.

How does the Fraction Mortgage compare to a HELOC for this purpose?

For diversification specifically, the Fraction Mortgage and a HELOC solve the liquidity problem differently. A HELOC requires monthly interest payments and income qualification, which means part of any equity you release immediately starts flowing back out as a servicing cost — and the Financial Consumer Agency of Canada warns that HELOC users who borrow more than they can afford risk "over-borrowing, debt persistence and wealth erosion," and that if you do not repay, "your lender may take possession of your home." The Fraction Mortgage requires neither a monthly payment nor mortgage-servicing income; instead, interest accrues and is settled at exit. The trade-off is that, with nothing paid down along the way, the amount owing on a Fraction Mortgage climbs until exit, whereas a HELOC borrower who pays monthly interest keeps the principal flat. Neither is "better" in the abstract — it depends on cash flow.

What are the risks of diversifying out of home equity?

The honest answer is that diversifying out of home equity uses leverage, and leverage cuts both ways. Three risks matter most. First, what you repay exceeds what you borrowed: because the Fraction Mortgage has no monthly payments, interest accrues daily and is added to the balance, so the lump sum settled at exit is larger than the amount advanced. Second, home prices fluctuate: CREA forecasts the national average home price at roughly $688,955 in 2026 (April 16, 2026 forecast), up just 1.5% and close to flat, with values having edged down 0.4% in late 2025 per Statistics Canada — releasing equity does not lock in today's value, and a falling market reduces the cushion between your loan and your home's worth. Third, like any mortgage, if the loan is not repaid during the repayment period, the homeowner risks foreclosure. Releasing equity to chase a higher return elsewhere only works if that return reliably exceeds the cost of the capital — which is never guaranteed. This is general information, not investment advice.

Is the cash from home equity release taxable in Canada?

Money you borrow is a loan, not income — so it is not taxed as income. That is true of all loans in Canada, including the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity does not create a taxable event, which is part of why equity release can be an efficient way to access concentrated housing wealth without triggering a sale. This is general information, not tax advice — consult a tax professional about your situation. You can read more about the tax framing of home equity cash and how it differs from liquidating other assets.

Who can use the Fraction Mortgage to diversify in BC, Ontario, and Alberta?

The Fraction Mortgage is available to owners of owner-occupied residential properties in British Columbia, Ontario, and Alberta, registered in a personal name. Fraction takes first position, so any existing mortgage is paid out from the proceeds, and lends up to 60% of the home's value. Qualification focuses on having enough income to service property taxes and other debts — not a mortgage payment, because there is not one — which makes it workable for self-employed and non-traditional-income owners. Credit-score minimums are 550 for the 1-year term and 660 for 3–5-year terms. Fraction can typically fund in 33 days. If you are weighing options, our guide to choosing a home equity release product in 2026 and the piece on reducing housing concentration risk walk through the decision.

Frequently asked questions

Which home equity release product helps diversify home equity in Canada?

The product best suited to diversifying home equity is one that releases a meaningful lump sum without forcing a sale and without a required monthly payment, so the cash stays available for other goals. In British Columbia, Ontario, and Alberta, the Fraction Mortgage is built for this: Fraction advances $100,000 to $1,000,000+ against the home, up to 60% of its value, and is due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying the balance. Because there is no monthly payment, the released equity is not eaten up by servicing costs. There is also no age restriction, unlike a reverse mortgage. The trade-off is that, since interest accrues daily and is settled in one lump sum at exit, the amount owing grows over the life of the loan. Whether diversification makes sense for you depends on your situation — consult a licensed professional.

How concentrated is Canadian household wealth in real estate?

Very concentrated. Statistics Canada's national balance sheet for the fourth quarter of 2025 (released March 16, 2026) valued household residential real estate at $8,450.6 billion against total household net worth of $18,594.9 billion — meaning real estate alone equals roughly 45% of all Canadian household net worth. For a typical owner without a large investment portfolio, the share is higher still, because the home is the one major asset most households buy with leverage and hold for decades. Statistics Canada also reported that real estate equalled 479.5% of household disposable income in Q4 2025. This concentration is the core reason diversification is worth considering: when most of your net worth rides on a single property in a single local market, your financial outcomes are unusually exposed to that one market's swings.

Why do homeowners struggle to access their home equity?

Homeowners struggle to access home equity because a house is an indivisible, illiquid asset — you cannot sell 10% of it to raise cash the way you can sell part of a stock holding. The traditional routes each carry friction: selling the whole property triggers moving costs and a new purchase, while borrowing options like a HELOC or cash-out refinance require monthly payments and income qualification, which not every owner can meet — especially the self-employed or retirees with strong assets but modest reported income. That is the "house-rich, cash-poor" squeeze: large net worth on paper, limited spendable cash. A no-monthly-payment product like the Fraction Mortgage addresses both barriers at once — it does not require you to sell, and it does not require mortgage-servicing income, because there is no monthly payment to qualify on. Fraction operates in BC, Ontario, and Alberta.

Can I diversify my wealth without selling my home?

Yes. The whole point of home equity release is to convert part of your housing wealth into cash while you keep the home and keep living in it. With the Fraction Mortgage, Fraction advances a lump sum against the property — up to 60% of its value — and you retain title. You can then hold a more balanced mix: some net worth still in the home, some in cash or other assets that move independently of your local housing market. This reduces the share of your wealth tied to a single property. Two caveats matter. First, releasing equity uses leverage, so it amplifies both gains and losses. Second, because there are no monthly payments, interest on the Fraction Mortgage accrues until exit and the balance owing rises over time. Whether to redeploy released equity into investments is a decision for a licensed financial professional, not something this article recommends.

Is the cash from home equity release taxable income in Canada?

No. Money you borrow is a loan, not income — so it is not taxed as income. That is true of all loans in Canada, including the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity does not create a taxable event. This is one reason equity release can be an efficient way to access concentrated housing wealth: you get usable cash without triggering a sale or realizing capital gains on other assets. Be careful with wording, though — the cash you receive is not taxable income, but that does not make it "free money"; it is a loan that must be repaid, with interest, at exit. And if you redeploy the funds into investments, the returns on those investments may themselves be taxable. This is general information, not tax advice — consult a tax professional about your specific situation.

How does diversifying out of home equity carry risk?

Diversifying out of home equity carries risk because it uses leverage, and leverage cuts both ways. Three risks stand out. First, you repay more than was advanced: with the no-monthly-payment Fraction Mortgage, interest accrues daily and is settled in one lump sum at exit, so the final payoff exceeds the original lump sum. Second, home prices fluctuate — CREA forecasts the 2026 national average home price at roughly $688,955, up just 1.5% and close to flat, and Statistics Canada recorded values edging down 0.4% in late 2025; releasing equity does not lock in today's price, and a falling market shrinks the cushion between your loan and your home's value. Third, as with any mortgage, if the loan is not repaid during the repayment period, the homeowner risks foreclosure. Redeploying equity to seek a higher return elsewhere only works if that return reliably beats the cost of the capital — which is never guaranteed.

How is the Fraction Mortgage different from a HELOC for diversification?

For diversification, the key difference is cash flow. A HELOC requires monthly interest payments and income qualification, so part of any equity you release immediately flows back out as a servicing cost — and the Financial Consumer Agency of Canada warns that HELOC users who borrow more than they can afford risk over-borrowing, debt persistence, and wealth erosion, and that if you do not repay, your lender may take possession of your home. The Fraction Mortgage requires neither a monthly payment nor mortgage-servicing income; interest accrues and is settled at exit instead. The trade-off is that, with nothing paid down in between, the amount owing on the Fraction Mortgage rises until exit, whereas a HELOC borrower who pays monthly interest keeps the principal flat. For an owner who wants released equity fully available to redeploy, the no-payment structure can be an advantage — but only if they are comfortable with a balance that climbs over time.

Can home equity release fund a second property?

Yes — funding a second property is one of the more common uses of released home equity, and it is a direct form of diversification when the second property is in a different market or serves a different purpose (for example, a rental). With the Fraction Mortgage, an owner can release a lump sum against an existing owner-occupied BC, Ontario, or Alberta home — up to 60% of its value — and use it toward the purchase of another, without taking on a monthly payment on the released amount. The Fraction Mortgage can even be used to purchase a home outright with 60% down and no monthly payments. As always, this spreads exposure across more than one property but also increases total leverage, so the math depends on rental income, carrying costs, and your timeline. Speak with a licensed mortgage professional before committing, and remember that with no payments in between, the Fraction balance compounds until exit.

Does diversifying with home equity require a minimum age?

No. The Fraction Mortgage has no age restriction — owners can qualify at any age, provided they meet the other requirements. This is a meaningful contrast with reverse mortgages, which in Canada are generally restricted to homeowners aged 55 and older. That makes home equity release through Fraction relevant to a wider group: a 40-year-old self-employed owner looking to free up capital, a 50-year-old consolidating debt, or a retiree bridging income. Qualification with Fraction focuses on having enough income to service property taxes and other debts — not a mortgage payment, because there is not one — along with a credit-score minimum of 550 for the 1-year term or 660 for the 3–5-year terms. Fraction lends only in British Columbia, Ontario, and Alberta, on residential properties registered in a personal name.

How much equity can I access without selling my home?

With the Fraction Mortgage you can generally access up to 60% of your home's value without selling, with loans ranging from $100,000 to $1,000,000 or more depending on your equity and property. Fraction takes first position, which means any existing mortgage is paid out from the proceeds and the remainder is advanced to you as a tax-free (because it is a loan, not income) lump sum. The amount you can access depends on the appraised value of the home, your existing mortgage balance, and Fraction's underwriting at the time. Because the goal of diversification is to release a useful amount of capital while leaving a healthy equity cushion in the home, most owners do not borrow the full 60% — leaving room reduces the risk that a market downturn erodes the buffer between the loan and the home's value. Fraction can typically fund in 33 days.

Does the Bank of Canada policy rate affect home equity release costs?

Indirectly, yes. The Bank of Canada held its policy interest rate at 2.25% on June 10, 2026, with the next scheduled announcement on July 15, 2026. The policy rate is the anchor for short-term borrowing costs across the economy, so it influences the pricing of HELOCs (which are typically tied to lenders' prime rates) and other equity products. The Fraction Mortgage offers options starting at 7.19% on a 3-year term (as of June 2026, subject to change) and a variable option tied to home appreciation with a set minimum and a capped maximum, priced using CORRA swap rates rather than directly off prime. For diversification planning, what matters most is the cost of the capital relative to whatever return you hope to earn by redeploying it — and rates can move, so today's pricing is not a forecast. Always confirm current rates with Fraction directly.

Which provinces does Fraction serve?

Fraction is a licensed mortgage lender operating only in British Columbia, Ontario, and Alberta. It is not available elsewhere in Canada. Within those three provinces, the Fraction Mortgage is offered on owner-occupied residential properties registered in a personal name (not a holding company). If you own a qualifying home in BC, Ontario, or Alberta and want to release equity to reduce your concentration in housing wealth — without selling and without a monthly payment — Fraction may be a fit. The process is 100% online: you can apply in minutes, get an estimate after a soft credit check that does not affect your score, and Fraction can typically fund in 33 days once the appraisal, knowledge quiz, and independent legal review are complete. This article is general information, not financial advice; speak with a licensed mortgage professional about your situation.

Sources

- Statistics Canada — National balance sheet and financial flow accounts, fourth quarter 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/260316/dq260316b-eng.htm

- Bank of Canada — Policy interest rate (key interest rate) — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- CREA — Downgrades resale housing market forecast (April 16, 2026) — https://www.crea.ca/media-hub/news/crea-downgrades-resale-housing-market-forecast-amid-tariff-uncertainty-and-economic-uncertainty/

- Financial Consumer Agency of Canada — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- Financial Consumer Agency of Canada — Home equity lines of credit — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/home-equity-line-credit.html

- Financial Consumer Agency of Canada — HELOCs: Market trends and consumer issues — https://www.canada.ca/en/financial-consumer-agency/programs/research/home-equity-lines-credit-trends-issues.html

- Capco — Equity Release: Seizing Opportunities, Navigating Risks — https://www.capco.com/intelligence/capco-intelligence/equity-release

This article is general information, not financial or tax advice. Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta (FSRA #13439; BCFSA #MB600547). Rates and figures are current as of June 2026, subject to qualification and change, and are not a commitment to lend. Speak with a licensed professional about your situation.