Choosing a Home Equity Release Product in Canada: The 2026 Decision Guide

A 2026 decision framework for choosing a Canadian home equity release product — compare HELOCs, reverse mortgages, refinances and Fraction on payments, eligibility, appreciation and cost.

Six decision dimensions — cash-flow tolerance, age, who captures home-price upside, repayment flexibility, eligible property, and total cost — that point you to the right home equity release product in BC, Ontario, or Alberta.

To choose a home equity release product in Canada, match the product to six things: your monthly cash-flow tolerance, your age, who captures home-price appreciation, repayment flexibility, your property type and province, and total cost. A HELOC, reverse mortgage, refinance, or the Fraction Mortgage each wins on a different dimension — there is no single best product.

Key takeaways

- There is no single best home equity release product — the right choice depends on which of six dimensions matters most to you: cash flow, age, appreciation exposure, repayment flexibility, property type, and total cost.

- If protecting monthly cash flow is the priority, products with no required monthly payment (the Fraction Mortgage, or a reverse mortgage for those 55+) fit better than a HELOC or refinance, which both add a monthly obligation.

- With the Bank of Canada policy rate held at 2.25% as of June 2026 and Canadian residential mortgage debt at $2.4 trillion (CMHC, December 2025), cash-flow pressure is the deciding factor for many homeowners this year.

- Most home equity products let you keep 100% of your home's future appreciation; shared-equity agreements trade a slice of that upside for cash today, which is the key trade-off to understand.

- The Fraction Mortgage is available on owner-occupied residential properties in British Columbia, Ontario, and Alberta, with no age restriction and no required monthly payment.

A home equity release product lets a Canadian homeowner turn part of their home's value into usable cash without selling. The hard part is not whether to release equity — it is choosing which product fits, because a HELOC, a reverse mortgage, a cash-out refinance, and the Fraction Mortgage each win on a different dimension. This guide is a decision framework, not a definition piece. (If you want the underlying definitions first, see how home equity release products work in Canada.)

The decision comes down to six questions. Work through them in order, and the field of options narrows quickly. The framework below gives each dimension an answer-first verdict, then a comparison table and a scenario matrix to map your situation to a product category.

What are the six dimensions for choosing a home equity release product?

The six dimensions that decide which home equity release product fits are: (1) your monthly cash-flow tolerance, (2) your age and eligibility constraints, (3) appreciation exposure — who captures your home's future price gains, (4) repayment flexibility and exit triggers, (5) eligible property type and province, and (6) total cost of capital including fees. No product wins all six. A HELOC offers low headline cost but demands monthly payments and income qualification. A reverse mortgage removes the payment but is restricted to homeowners 55 and older. The Fraction Mortgage removes the required monthly payment with no age restriction but, like any non-amortizing loan, lets the balance grow over time. The right answer is whichever product wins the one or two dimensions that matter most to you.

Does protecting your monthly cash flow point to a no-payment product?

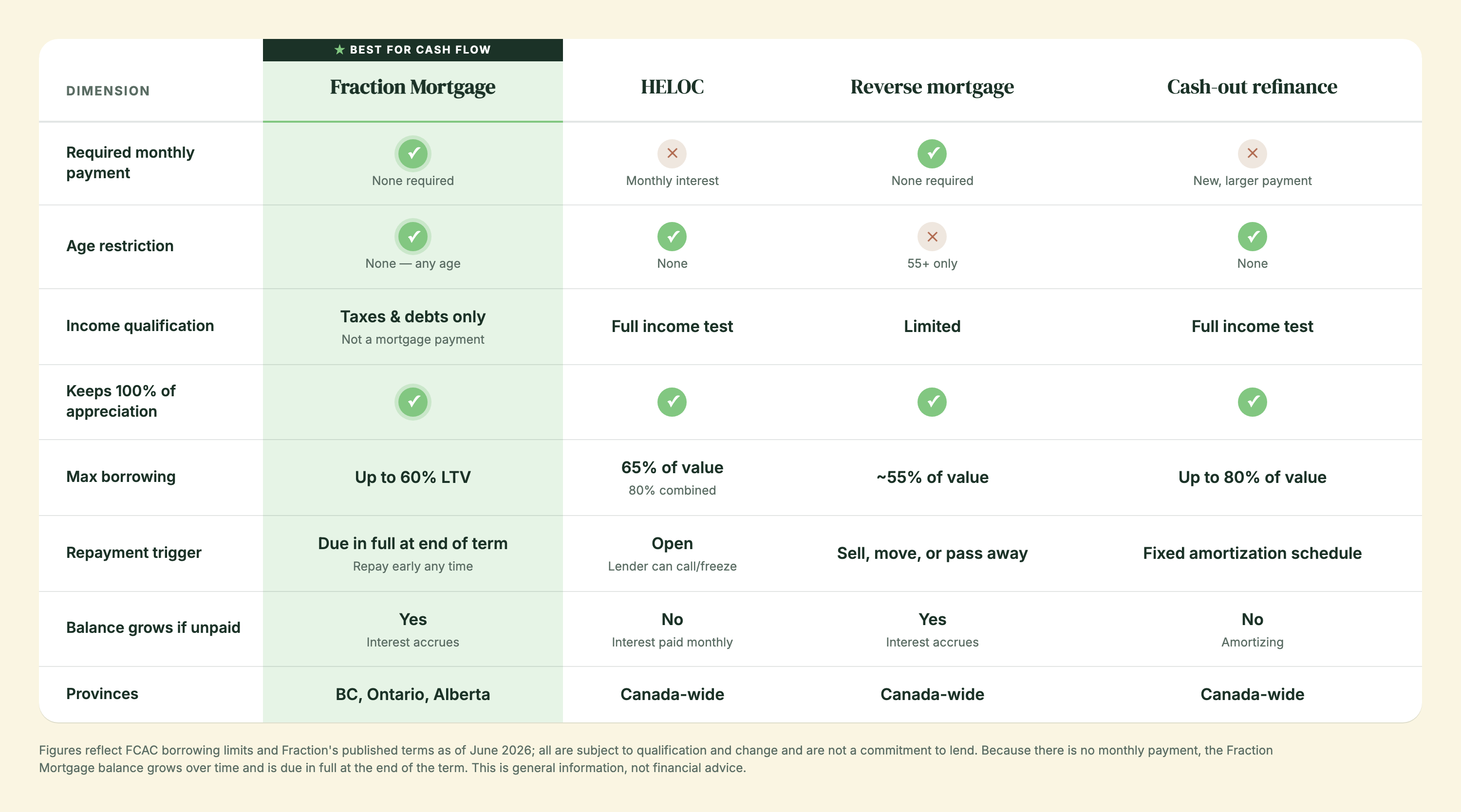

Yes — if monthly cash flow is your binding constraint, a product with no required monthly payment is the strongest fit. A HELOC and a cash-out refinance both add a monthly obligation: a HELOC requires monthly interest payments, and a refinance creates a new, larger amortizing payment. By contrast, the Fraction Mortgage has no required monthly payment — interest accrues daily and is due in full at the end of the term, settled in one lump sum — by selling, refinancing with another lender, or repaying (early repayment is allowed). A reverse mortgage similarly requires no monthly payment, but only for those 55 and older.

This dimension is especially live in 2026. The Bank of Canada held its policy rate at 2.25% again at its June 10, 2026 decision, and the C.D. Howe Institute's Monetary Policy Council recommended the Bank "keep its target for the overnight rate at 2.25 percent at its next announcement on June 10, maintain it at that level until December of this year, and raise it to 2.5 percent by June 2027." The Bank did exactly that on June 10, holding at 2.25%. Rates are no longer falling — so adding a new monthly payment on top of an existing mortgage is a heavier decision than it was two years ago. For homeowners with strong equity but tight monthly budgets, removing the payment is often worth more than shaving the headline rate.

$2.4T — in Canadian residential mortgage debt as of December 2025, up 4.8% year over year — CMHC, mortgage market update

CMHC also reported the national 90-plus-day mortgage delinquency rate rising to 0.24% in the fourth quarter of 2025 (from 0.21% a year earlier), with arrears up 35% year over year in Ontario and 45% in the Toronto area. For a household feeling that pressure, releasing equity without adding another payment can be the difference between staying put and being forced to sell. See no-monthly-payment home equity options in Canada for the full comparison.

Does your age rule any home equity release products in or out?

Age is a hard gate on one product and a non-factor on the others. A reverse mortgage in Canada is restricted to homeowners 55 and older — below that age, it is simply not available. A HELOC, a cash-out refinance, and the Fraction Mortgage have no upper or lower age restriction; they qualify on equity, property, and credit rather than birthdate. The Fraction Mortgage states plainly that homeowners can "qualify at any age," which is the key contrast with reverse mortgages for borrowers in their 40s and 50s who want a no-payment structure but are years away from the reverse-mortgage threshold.

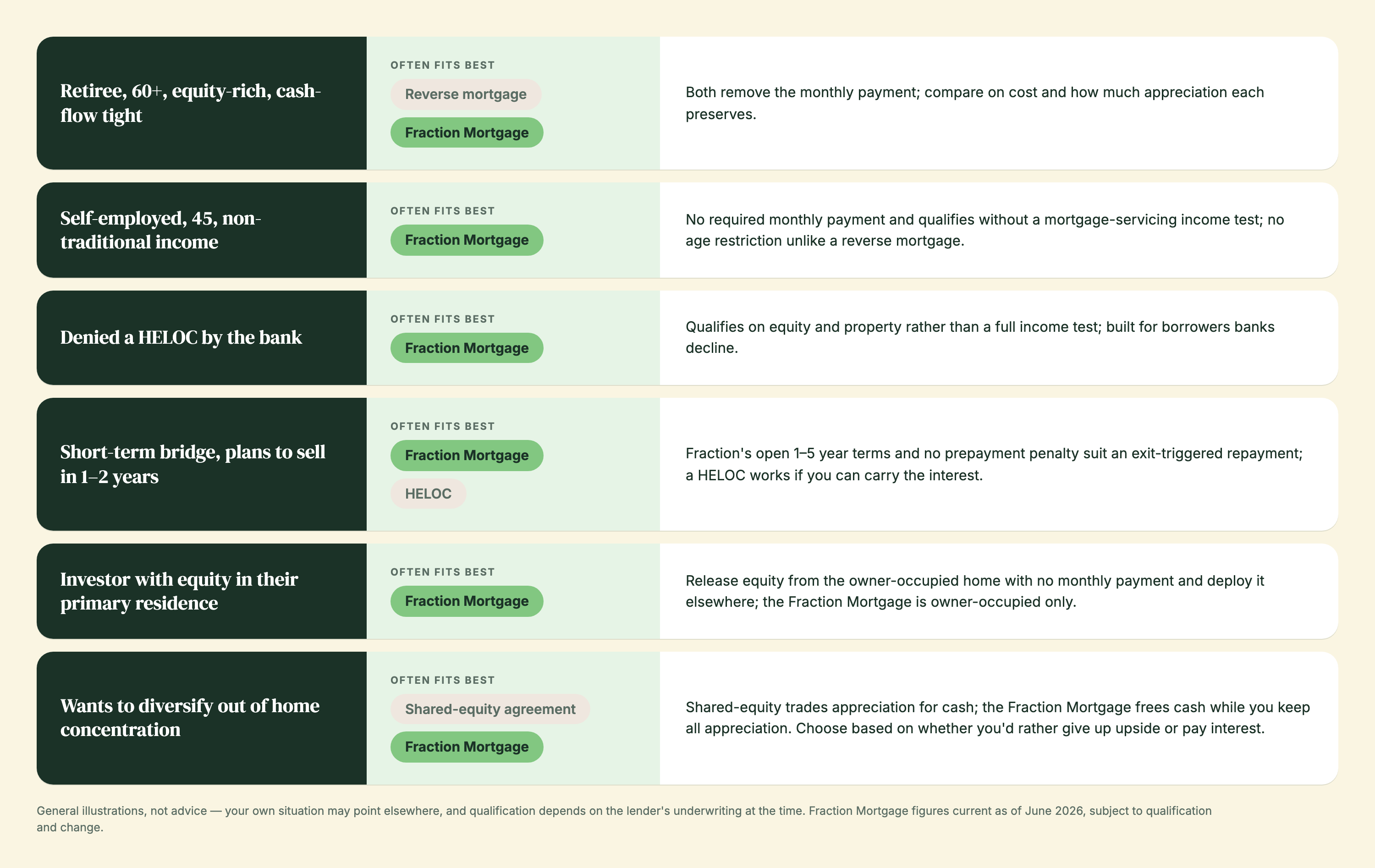

Practically, this means a 48-year-old self-employed homeowner who wants payment-free access to equity cannot use a reverse mortgage, but can consider the Fraction Mortgage. A 70-year-old retiree, by contrast, has both no-payment options open and should compare them on cost and how much of their home's appreciation each one preserves. For more on diversifying away from a single concentrated asset, see how home equity investment can diversify housing wealth.

Who captures your home's future appreciation under each product?

With most home equity release products, the homeowner keeps 100% of future appreciation — the lender is owed principal plus interest, nothing more. That is true of a HELOC, a cash-out refinance, and the Fraction Mortgage: the homeowner retains title and captures all future price gains on the property. The single biggest exception is a shared-equity (home equity sharing) agreement, where an investor advances cash today in exchange for a share of the home's future value — meaning the homeowner gives up a slice of appreciation rather than paying interest. This is the central trade-off in the "diversification" framing some products use.

This dimension is where Canadian household balance sheets come into focus. Statistics Canada reported household residential real estate worth roughly $8.5 trillion ($8,499.4 billion) against total household net worth of $18.4 trillion in the third quarter of 2025 — making the principal residence the largest non-financial asset for most households. A homeowner who is heavily concentrated in their home may rationally trade some appreciation for diversification through a shared-equity product; one who expects strong local price growth and wants to keep all of it should favour a loan-style product like the Fraction Mortgage, whose cost is interest, not a share of the upside.

$8.5T — value of Canadian household residential real estate in Q3 2025, against $18.4T in total household net worth — Statistics Canada, national balance sheet accounts

How much repayment flexibility and which exit triggers do you need?

Repayment flexibility separates open, exit-triggered products from fixed-schedule ones. A HELOC is flexible to draw and repay but charges monthly interest and can be called or frozen by the lender. A cash-out refinance locks you into a fixed amortization schedule, often with a prepayment penalty for breaking early. A reverse mortgage and the Fraction Mortgage are repaid at an exit event rather than on a monthly schedule. The Fraction Mortgage offers open terms of 1–5 years, is fully open with no prepayment penalties (after the first 8 months), and is due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying directly — there are no partial payments, just the full balance at exit.

The trade-off to state plainly: because there is no monthly payment, the Fraction Mortgage balance grows over time as interest accrues. And as with any mortgage, if the loan is not repaid during the repayment period, the homeowner risks foreclosure. That honesty is part of the decision — a no-payment product is not a no-cost product. Near term-end, Fraction sends a letter roughly 90 days before expiry, and the options are to sell and repay, or repay the balance directly.

Is your property type and province eligible?

Eligibility by property and location can eliminate a product before any other dimension matters. The Fraction Mortgage is available on owner-occupied residential properties in British Columbia, Ontario, and Alberta, registered in a personal name (not a holding company). It can be used to access equity in an existing home, or to purchase a home with 60% down and no monthly payments. HELOCs, refinances, and reverse mortgages are broadly available across Canada, but underwriting varies by lender, property type, and — for HELOCs and refinances — your income and credit.

A key planning point set by the Financial Consumer Agency of Canada (FCAC): with a HELOC you may borrow up to 65% of your home's value, but your mortgage plus HELOC combined cannot exceed 80%; a home equity loan can reach up to 80%; and a reverse mortgage usually allows up to about 55% of appraised value. The Fraction Mortgage advances up to 60% loan-to-value, from $100,000 up to $1,000,000 or more depending on equity and property, in first position — meaning any existing mortgage is paid out from the proceeds. If you own a condo in Calgary, a townhouse in Toronto, or a house in Vancouver and want a no-payment structure, the province and property-type fit is a fast way to shortlist.

What is the total cost of capital, including fees?

Total cost is the dimension homeowners most often underestimate, because the headline rate is only part of it. For the Fraction Mortgage, the published structure (as of June 2026, subject to change) is options starting at 7.19% on a 3-year term, or a variable rate tied to home appreciation with a set minimum and a capped maximum, priced off CORRA swap rates. Fraction's origination fee (starting at 3%), independent legal representation (est. $2,250), and conveyancing including title insurance (approximately $1,850 + est. $500) are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal ($400–$600), plus a home inspection if the loan amount is over $1,000,000. A HELOC typically has a lower headline rate but adds the carrying cost of monthly interest and income-qualification friction; a refinance can trigger a prepayment penalty on the mortgage you break.

The right way to compare is total cost over your expected holding period, not the rate alone. A product with a slightly higher rate but no required monthly payment can preserve more cash flow than a cheaper product you must service every month — particularly relevant given the 2026 rate environment and household debt loads. Statistics Canada pegged the household debt-to-income ratio at 176.7% in Q3 2025 — there was $1.77 in credit-market debt for every dollar of disposable income — so for many households the binding cost is monthly affordability, not the posted rate. For a deeper read on cost trade-offs, see the Fraction Mortgage and tax-free access to equity.

176.7% — Canadian household debt-to-income ratio in Q3 2025 — $1.77 of debt for every dollar of disposable income — Statistics Canada, national balance sheet accounts

How do the main home equity release products compare side by side?

The table below compares the four main Canadian home equity release categories on the dimensions that drive the decision. Figures reflect FCAC borrowing limits and Fraction's published terms as of June 2026; all are subject to qualification and change.

Which product fits which homeowner scenario?

The decision matrix below maps common Canadian homeowner scenarios to the product category that typically fits best, and why. These are general illustrations, not advice — your own situation may point elsewhere, and qualification depends on the lender's underwriting at the time.

If a bank declined you, the relevant gate is usually income or product fit, not your home's equity. The Fraction Mortgage's credit-score minimums are 550 on a 1-year term and 660 on 3–5-year terms (using your Beacon/credit score), and it requires enough income to service property taxes and other debts — not a mortgage payment, because there isn't one. For the full decision around bank declines, read how to reduce housing risk with home equity access and compare the options above alongside Fraction's own why Fraction and cost pages.

Is the cash from a home equity release product taxable in Canada?

Money you borrow is a loan, not income — so it isn't taxed as income. That is true of all loans in Canada, including the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity doesn't create a taxable event. This is one reason homeowners reach for an equity release product instead of selling an asset: a sale can crystallize a gain, while a loan generally does not. This is general information, not tax advice — consult a tax professional about your situation. The CREA national average home price reached roughly $695,412 in April 2026 (up 2.2% year over year), so for many Canadians the equity available to release is substantial — which makes the tax framing worth understanding before you choose a product.

How does the 2026 rate environment change the decision?

In 2026, the deciding dimension for many homeowners has shifted from "lowest rate" to "lowest monthly burden." With the Bank of Canada policy rate steady at 2.25% as of June 2026 and not expected to fall further this year, the era of refinancing into a cheaper payment is largely over. CMHC's latest figures show $2.4 trillion in residential mortgage debt outstanding as of December 2025, up 4.8% year over year, and a 90-plus-day delinquency rate that ticked up to 0.24% in the fourth quarter — with arrears rising fastest in Ontario (up 35% year over year) and the Toronto area (up 45%). For a household whose budget is already stretched, layering on a HELOC's monthly interest or a refinance's larger payment can be the wrong move, even at a low rate. That is why no-payment products — the Fraction Mortgage at any age, or a reverse mortgage for those 55+ — are getting a closer look this year. The framework still holds: rank the six dimensions for your situation, and let cash-flow tolerance carry more weight in a flat-rate environment with rising debt-servicing strain.

Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta. FSRA #13439 (Ontario) · BCFSA #MB600547 (British Columbia). This article is general information, not financial advice — speak with a licensed mortgage professional about your situation. Rate and cost examples are as of June 2026, subject to qualification and change, and are not a commitment to lend.

Frequently asked questions

Which home equity release product helps diversify home equity?

Two product categories help a homeowner diversify out of concentrated home wealth, and they work differently. A shared-equity (home equity sharing) agreement gives an investor a share of your home's future value in exchange for cash today, directly trading appreciation for diversification. A loan-style product like the Fraction Mortgage frees up cash you can invest elsewhere while you keep 100% of your home's future appreciation — the cost is interest rather than a share of the upside. Which fits depends on whether you would rather give up some price gains (shared equity) or carry an interest cost (a loan). Statistics Canada reported about $8.5 trillion of household wealth tied up in residential real estate in Q3 2025, so diversification is a real goal for equity-rich, cash-poor households. The Fraction Mortgage is available on owner-occupied properties in BC, Ontario, and Alberta with no required monthly payment.

What is the best home equity release product in Canada?

There is no single best home equity release product — the right one depends on which of six dimensions matters most: monthly cash-flow tolerance, age, who captures appreciation, repayment flexibility, eligible property and province, and total cost. A HELOC offers a lower headline rate but requires monthly interest and income qualification. A reverse mortgage removes the payment but is limited to homeowners 55 and older. A cash-out refinance can consolidate debt but creates a new, larger monthly payment. The Fraction Mortgage removes the required monthly payment with no age restriction, available in BC, Ontario, and Alberta, while letting the homeowner keep all future appreciation. Rank the six dimensions for your situation, and the strongest fit usually becomes clear. Because Fraction has no monthly payment, the balance grows over time — a trade-off to weigh against the cash-flow benefit.

How do I choose between a HELOC and a no-monthly-payment product?

Choose by your cash-flow tolerance and income qualification. A HELOC typically carries a lower headline rate but requires monthly interest payments and a full income test, and the lender can reduce or freeze it. A no-monthly-payment product like the Fraction Mortgage requires no monthly payment — interest accrues and is due in full at the end of the term — settled by selling, refinancing with another lender, or repaying — and qualifies on equity rather than a mortgage-servicing income test. If you have steady income and want the lowest carrying cost, a HELOC may win on total cost. If your income is variable or self-employed, or if your monthly budget is already stretched, the no-payment structure usually fits better. With the Bank of Canada policy rate held at 2.25% as of June 2026 and Canadian residential mortgage debt at $2.4 trillion (CMHC, December 2025), monthly affordability is the deciding factor for many homeowners this year.

Can I release home equity if a bank denied me a HELOC?

Yes — being declined for a HELOC usually reflects income or product fit, not a lack of home equity. Banks apply a full income test to HELOCs and refinances, which often catches self-employed borrowers, those with non-traditional income, or anyone whose debt servicing looks tight on paper. The Fraction Mortgage qualifies on equity and property rather than requiring income to service a mortgage payment, because there is no monthly payment to service — only enough income to cover property taxes and other debts. Its credit-score minimums are 550 on a 1-year term and 660 on 3–5-year terms (using your Beacon/credit score). It lends up to 60% loan-to-value on owner-occupied residential properties in British Columbia, Ontario, and Alberta. So a bank decline does not close the door; it often points toward a different product category designed for exactly that situation.

Who keeps the home's appreciation under a home equity release product?

With most home equity release products, the homeowner keeps 100% of future appreciation. That includes a HELOC, a cash-out refinance, and the Fraction Mortgage — the lender is owed principal plus interest only, and the homeowner retains title and all future price gains. The main exception is a shared-equity agreement, where an investor takes a share of the home's future value in exchange for the upfront cash, so the homeowner gives up part of the appreciation rather than paying interest. This is the central decision in the appreciation dimension: if you expect strong local price growth and want to keep all of it, favour a loan-style product whose cost is interest; if you want to diversify and are comfortable trading some upside for cash, a shared-equity product may fit. Statistics Canada reported Canadian residential real estate worth about $8.5 trillion in Q3 2025, so appreciation exposure is a meaningful sum for most owners.

What does a home equity release product cost in total?

Total cost is the rate plus fees plus the carrying cost over your holding period — not the headline rate alone. For the Fraction Mortgage as of June 2026 (subject to change), the published structure is options starting at 7.19% on a 3-year term, or a variable rate tied to home appreciation with a set minimum and a capped maximum, priced off CORRA swap rates. Fraction's origination fee (starting at 3%), independent legal representation (est. $2,250), and conveyancing including title insurance (approximately $1,850 + est. $500) are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal ($400–$600), plus a home inspection if the loan amount is over $1,000,000. A HELOC often shows a lower rate but adds monthly interest you must carry; a refinance can trigger a prepayment penalty on the mortgage you break. Compare on total cost over the time you plan to hold the loan, and weigh whether removing a monthly payment is worth a higher rate for your cash flow. Figures are illustrative and subject to qualification and change; this is not a commitment to lend.

Is there an age limit on home equity release products in Canada?

Age is a hard limit on one product only. A reverse mortgage in Canada is restricted to homeowners 55 and older — it is unavailable below that age. A HELOC, a cash-out refinance, and the Fraction Mortgage have no age restriction; they qualify on equity, property, and credit instead. The Fraction Mortgage explicitly lets homeowners qualify at any age, which is its key contrast with a reverse mortgage for borrowers in their 40s and 50s who want a no-payment structure but are too young for a reverse mortgage. So if your priority is no monthly payment and you are under 55, the reverse mortgage is off the table, but the Fraction Mortgage remains an option. If you are 55 or older, both no-payment options are open, and the decision shifts to total cost and how much of your home's appreciation each one preserves.

What property types and provinces qualify for the Fraction Mortgage?

The Fraction Mortgage is available on owner-occupied residential properties in British Columbia, Ontario, and Alberta, registered in a personal name rather than a holding company. It lends in first position, meaning any existing mortgage is paid out from the proceeds, up to 60% loan-to-value, from $100,000 up to $1,000,000 or more depending on equity and property. It can release equity from an existing home or fund a purchase with 60% down and no monthly payments. If your property is outside BC, Ontario, or Alberta, the Fraction Mortgage is not available — but other Canada-wide products such as a HELOC, refinance, or reverse mortgage may fit. Always confirm current eligibility, because underwriting requirements can change.

How much equity can I access with each product?

Borrowing limits differ by product, and the Financial Consumer Agency of Canada (FCAC) sets the standard reference points. With a HELOC you may borrow up to 65% of your home's value, but your mortgage plus HELOC combined cannot exceed 80%. A home equity loan can reach up to 80% of value. A reverse mortgage usually allows up to about 55% of appraised value. The Fraction Mortgage advances up to 60% loan-to-value, from $100,000 up to $1,000,000 or more depending on your equity and property. So a homeowner who needs the maximum dollar amount and can service monthly payments may get more from a HELOC-plus-mortgage or a refinance; a homeowner who wants no monthly payment trades a slightly lower ceiling for that flexibility. Match the limit to how much you actually need rather than the highest available — borrowing more than necessary raises your cost and, for non-amortizing products, the balance that grows over time.

When does a home equity release product have to be repaid?

Repayment timing depends on the product's exit trigger. A cash-out refinance is repaid on a fixed amortization schedule, with monthly payments and often a penalty for breaking early. A HELOC is open — you can draw and repay flexibly — but you pay interest monthly and the lender can call or freeze the line. A reverse mortgage is repaid when you sell, move out permanently, or pass away. The Fraction Mortgage offers open terms of 1–5 years and is due in full at the end of the term — repaid by selling, refinancing with another lender, or repaying directly; it is fully open with no prepayment penalties (after the first 8 months), but there are no partial payments — it is the full balance at exit. Near term-end, Fraction sends a letter roughly 90 days before expiry, and the options are to sell and repay, or repay the balance directly. As with any mortgage, if a Fraction Mortgage is not repaid during the repayment period, the homeowner risks foreclosure — a downside worth stating plainly.

Does the 2026 interest-rate environment change which product I should choose?

Yes — in 2026 the deciding dimension has shifted from lowest rate to lowest monthly burden for many homeowners. The Bank of Canada held its policy rate at 2.25% as of June 2026, and the C.D. Howe Institute's Monetary Policy Council recommended holding at 2.25% on June 10 and through December before any move to 2.5% by June 2027. With rates no longer falling, the case for refinancing into a cheaper payment has weakened. At the same time, CMHC reported $2.4 trillion in residential mortgage debt outstanding as of December 2025 (up 4.8% year over year) and a rising delinquency rate. For a household whose budget is already stretched, adding a HELOC's monthly interest or a refinance's larger payment can be the wrong move even at a low rate. That tilts the decision toward no-payment products — the Fraction Mortgage at any age, or a reverse mortgage for those 55 and older. The six-dimension framework still applies; cash-flow tolerance simply carries more weight in a flat-rate environment.

Sources

- Bank of Canada — Policy interest rate — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- C.D. Howe Institute — Monetary Policy Council, June 2026 — https://cdhowe.org/publication/mpcjune2026/

- CMHC — Renewal wave peaks but still dominates mortgage market (2026) — https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2026/renewal-wave-peaks-still-dominates-mortgage-market

- Statistics Canada — National balance sheet and financial flow accounts, Q3 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/251211/dq251211a-eng.htm

- Financial Consumer Agency of Canada — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- CREA — MLS Home Price Index and April 2026 statistics — https://stats.crea.ca/en-ca/

This article is general information, not financial or tax advice. Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta (FSRA #13439; BCFSA #MB600547). Rates and figures are current as of June 2026, subject to qualification and change, and are not a commitment to lend. Speak with a licensed professional about your situation.